مقال إخباري

مقياس الربع الرابع من عام 2022 QIMA 2022

4 أكتوبر 2022

بارومتر الربع الرابع من عام 2022: موسم عطلات مضطرب آخر في المتجر بالنسبة للمصادر العالمية

بعد مرور ثلاثة أرباع من عام 2022، تُظهر بيانات معهد قطر لبحوث الاقتصاد الإسلامي أن مشهد التوريد العالمي لا يزال في حالة تغير مستمر، مع تعمق انفصال سلاسل التوريد العالمية عن الصين واحتدام المنافسة بين أسواق التوريد الأخرى في آسيا، في حين أن شبح الركود في الغرب يؤثر على ثقة المستهلكين وحجم مشترياتهم.

تشير هذه الاتجاهات، بالإضافة إلى الاضطرابات المستمرة بسبب تدابير احتواء كوفيد-19 التي اتخذتها الصين، والكوارث الطبيعية التي تهدد مناطق المواد الخام الرئيسية والاضطرابات الجيوسياسية المستمرة، إلى أن المصادر العالمية قد تتجه نحو موسم عطلات مضطرب آخر.

التضخم والجغرافيا السياسية وعمليات الإغلاق تتضافر معًا لمواصلة دفع المشترين الغربيين إلى الابتعاد عن الصين

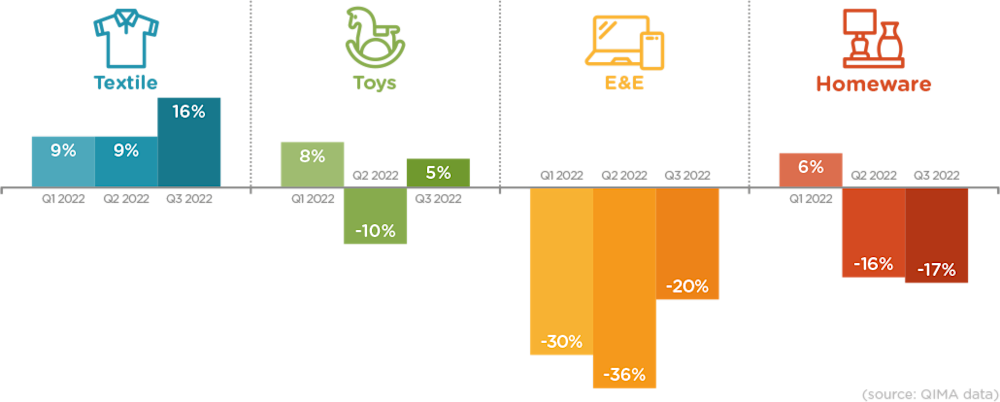

تُظهر بيانات معهد قطر لبحوث الاقتصاد الإسلامي حول الطلب على الفحص والتدقيق أنه خلال الربع الثالث من عام 2022، استمر الاهتمام بالتوريد المصنوع في الصين بين المشترين الغربيين في الانكماش بنفس الوتيرة التي شهدها النصف الأول من عام 2022. انخفض الطلب على الفحص والتدقيق من المشترين في الولايات المتحدة والاتحاد الأوروبي بنسبة -5% على أساس سنوي في الربع الثالث، مما يعكس معنويات المستهلكين المخنوقة بالتضخم في الولايات المتحدة والاتحاد الأوروبي، واستمرار فصل سلاسل التوريد الغربية عن الصين، والتأثير التخريبي المستمر لعمليات الإغلاق بسبب فيروس كورونا المستجد (كوفيد-19)، على الرغم من الآمال السابقة بأن انتقال الصين إلى سياسة "ديناميكية خالية من فيروس كورونا" سيخفف من عبء احتواء الفيروس على التصنيع. لا يزال قطاع الكهرباء والإلكترونيات من بين القطاعات الأكثر تضررًا، ما بين النقص المستمر في أشباه الموصلات والتحول المتزايد في مصادر التكنولوجيا إلى منافسي الصين، بما في ذلك فيتنام وماليزيا ومؤخرًا الهند.

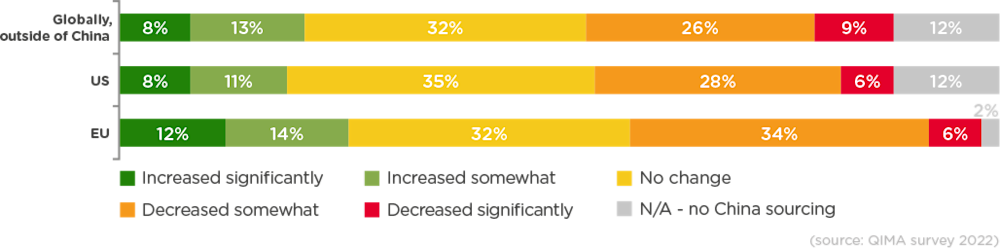

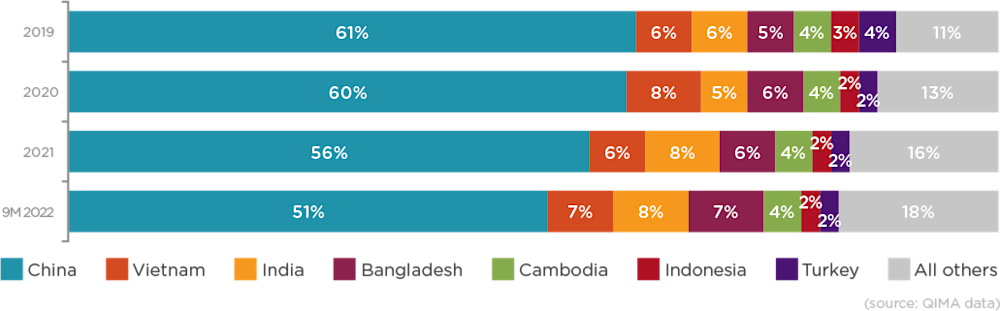

ومع ذلك، عند وضع هذا الأمر في منظوره الصحيح، فإن ابتعاد المشترين الغربيين عن الصين لا يزال بطيئاً: في حين أن أكثر من ثلثي المشاركين في استطلاع معهد قطر لبحوث الصناعة والتجارة الدولية لعام 2022 أفادوا بعدم زيادة الشراء من الموردين الصينيين في عام 2022 مقارنة بعام 2021، فإن 6٪ فقط خفضوا مصادرهم من الصين بشكل كبير. في تجاور مماثل يوضح الأهمية المستمرة للصين بالنسبة لسلاسل التوريد الغربية، تُظهر بيانات QIMA حول عمليات التفتيش والتدقيق أن حصة الصين بين أهم أسواق التوريد للمشترين الغربيين في أدنى مستوياتها منذ أربع سنوات - لكن ما يقرب من 90% من المشاركين في الاستطلاع من الولايات المتحدة والاتحاد الأوروبي لا يزالون يسمون الصين كأحد أهم 3 شركاء شراء لهم.

الشكل C1. أبلغت العلامات التجارية وتجار التجزئة عن تغييرات في أحجام التوريد إلى الصين في عام 2022 مقارنة بعام 2021 (المصدر: مسح معهد قطر لبحوث الاقتصاد الإسلامي)

الشكل ج2. أهم أسواق التوريد للمشترين من الولايات المتحدة والاتحاد الأوروبي حسب الحصة (المصدر: بيانات معهد قطر لبحوث الاقتصاد الإسلامي)

الشكل C3. ديناميكية النمو السنوي للتفتيش والتدقيق في الصين خلال عام 2022: صناعات مختارة (المصدر: بيانات QIMA)

فيتنام تعود أخيرًا إلى اللعبة وتحول الانتعاش المؤقت إلى نمو مستدام في الربع الثالث من العام

بعد أن شهدت فيتنام تراجعًا في النصف الأول من عام 2022 بسبب نقص الموظفين وتراجع الطلب، يبدو أن فيتنام تستعيد ثقة المشترين في النصف الثاني من عام 2022. بعد الانتعاش الأولي الذي شهده التصنيع الفيتنامي نجح في تسخير الزخم في استمرار النمو خلال الربع الثالث، حيث ارتفع الطلب على عمليات التفتيش والتدقيق من العلامات التجارية التي تتخذ من الولايات المتحدة مقراً لها بنسبة +59% على أساس سنوي في الربع الثالث، وتضاعف أكثر من الضعف من العلامات التجارية الأوروبية. تُظهر بيانات QIMA أن تدفق الأعمال الجديدة إلى فيتنام كان واضحًا بشكل خاص في شهر أغسطس، تزامنًا مع موجة أخرى من عمليات الإغلاق في الصين.

الشكل V1: ديناميكية النمو السنوي للطلب على التفتيش والتدقيق في فيتنام في عام 2022 (المصدر: بيانات معهد قطر لبحوث الاقتصاد الإسلامي)

كما دخلت وجهات التوريد الأخرى في جنوب شرق آسيا في النصف الثاني من عام 2022 على أسس قوية، حيث أظهرت بيانات معهد قطر لبحوث الاقتصاد الإسلامي توسعاً مضاعفاً في الطلب على الفحص والتدقيق في إندونيسيا وتايلاند وماليزيا عبر فئات متعددة من المنتجات. يتم النظر إلى ماليزيا على وجه الخصوص بشكل متزايد في ماليزيا من أجل توريد منتجات الطاقة والكهرباء مع قيام العلامات التجارية العالمية للتكنولوجيا بتحويل أحجام التصنيع من الصين.

وتيرة النمو في الهند تستقر بعد فترة من التوسع الهائل

بعد عدة أرباع متتالية من التوسع الهائل على أساس سنوي، يبدو أن التوريد في الهند يستقر في وتيرة نمو أكثر استدامة، حيث ارتفع الطلب على عمليات الفحص والتدقيق الآن بنسبة +13% على أساس سنوي في 9 أشهر من عام 2022 (مقارنةً بنمو +41% على أساس سنوي في النصف الأول من عام 2022). يمكن أن يعزى بعض هذا التباطؤ إلى ارتفاع التضخم في الاتحاد الأوروبي والولايات المتحدة الذي يضعف طلب المستهلكين على السلع غير الأساسية، والتي تشمل الملابس وخاصة الأدوات المنزلية.

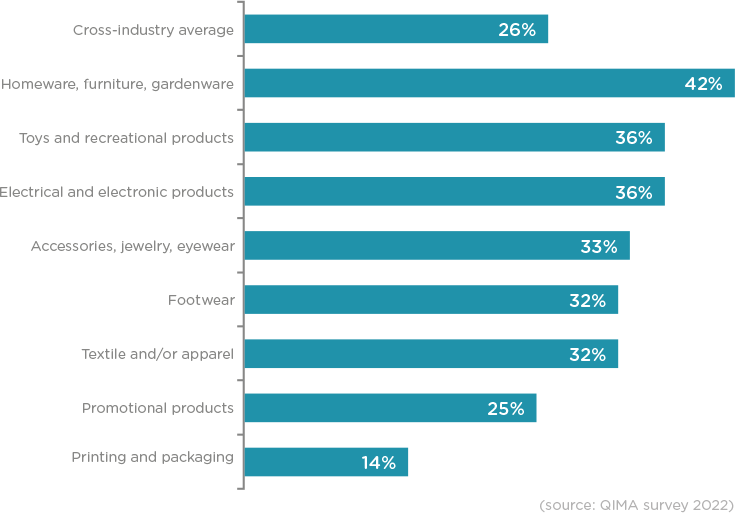

ومع ذلك، وعلى الرغم من أهمية هذه الفئات من المنتجات بالنسبة لصادرات الهند، فإن التوريد إلى الهند لا يبدأ وينتهي بالمنسوجات: كما يتضح من الاهتمام المتزايد من العلامات التجارية الكبرى للإلكترونيات، ومن بينها Apple وGoogle، بقدرات التصنيع الهندية. وقد وجد استطلاع معهد قطر لبحوث الاقتصاد الإسلامي أن أكثر من ثلث المشاركين في الاستطلاع من العاملين في قطاع الإلكترونيات والإلكترونيات وسّعوا نطاق مصادرهم في الهند في عام 2022.

وتعاني بلدان أخرى في المنطقة من التحديات الخاصة بها، بدءًا من الأزمة الاقتصادية المستمرة في سريلانكا إلى الفيضانات المدمرة في باكستان التي دمرت نصف محاصيل القطن في البلاد تقريبًا. وقد ساهم كل ذلك، بالإضافة إلى التباطؤ في الطلبات من الغرب، في التوسع المتواضع نسبيًا بنسبة +10% على أساس سنوي في الفحص والطلب في منطقة جنوب آسيا ككل.

الشكل الأول 1. الشركات التي أبلغت عن توسيع مصادر توريدها للهند في عام 2022 - حسب الصناعة (مسح معهد قطر لبحوث الاقتصاد الإسلامي)

تشهد المناطق القريبة من الحدود اهتمامًا مستدامًا كلاعبين داعمين

في الرحلة المستمرة نحو تنويع مصادر التوريد، لا تزال العلامات التجارية الغربية وتجار التجزئة يوسعون نطاق مشترياتهم في مناطقهم القريبة من التوريد. في منطقة البحر الأبيض المتوسط، شهدت تركيا والمغرب على التوالي نموًا بنسبة 26% على أساس سنوي و24% على أساس سنوي في أحجام الفحص والتدقيق من العلامات التجارية في الاتحاد الأوروبي في 9 أشهر من عام 2022؛ بينما عبر المحيط الأطلسي، شهدت كل من المكسيك وغواتيمالا توسعًا مضاعفًا في الطلب على الفحص والتدقيق من المشترين في الولايات المتحدة خلال الفترة الزمنية نفسها. وفي حين أن هذا الاتجاه يؤكد دورهما كمكونين مهمين في استراتيجية تنويع سلاسل التوريد، إلا أن الأحجام المشتراة من المناطق القريبة من التوريد لا يزال أمامها طريق طويل قبل أن تصل إلى حجم التوريد الخارجي.

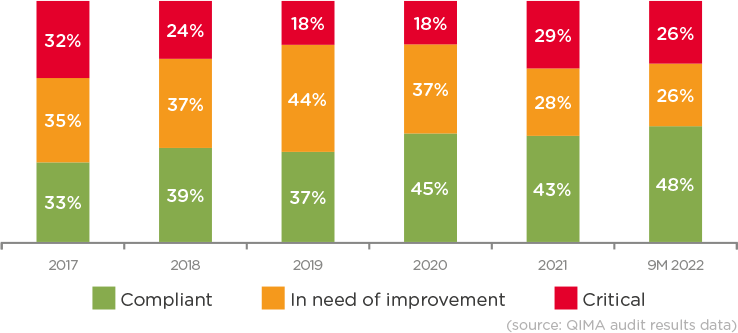

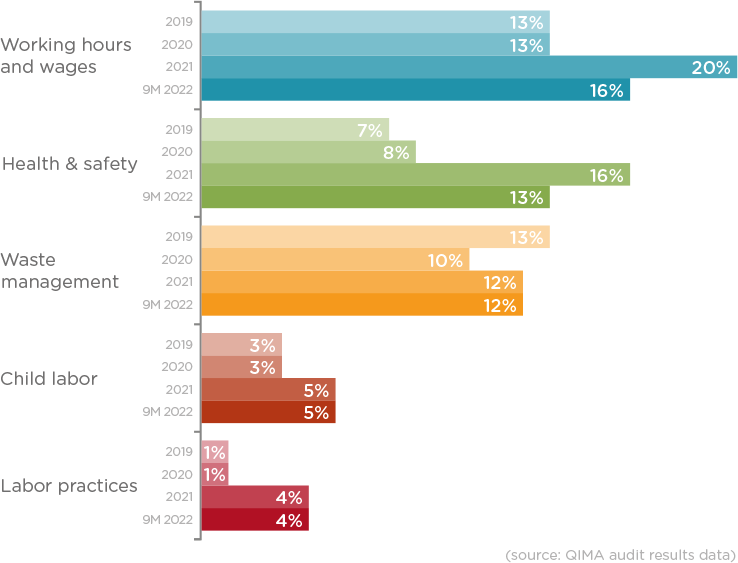

الانتهاكات الخطيرة في أخلاقيات سلسلة التوريد تتجاوز مستويات ما قبل الجائحة

تُظهر البيانات التي جمعها مدققو الأخلاقيات في معهد قطر لبحوث الصناعة والأمن الغذائي خلال عمليات التدقيق الميداني في عام 2022 أن الامتثال الأخلاقي في سلاسل التوريد لم يبدأ بعد في التعافي من التدهور الحاد الذي شهده مع بداية الجائحة. ففي أربعة من المجالات الرئيسية الخمسة التي قيّمها مدققو معهد قطر لبحوث البيئة والموارد الطبيعية في عام 2022، كانت النسبة المئوية للمصانع التي ارتكبت انتهاكات جسيمة في عام 2022 أعلى بشكل ملحوظ من مستويات عام 2019. ومن المثير للقلق أن احتمال عدم الامتثال الحرج المتعلق بعمالة الأطفال قد تضاعف تقريباً في عام 2022 مقارنة بفترة ما قبل الجائحة.

مع وجود أكثر من نصف المصانع التي خضعت للتدقيق في حاجة إلى تحسين فوري أو قريب الأجل للامتثال الأخلاقي، هناك حاجة حقيقية للعلامات التجارية وتجار التجزئة لاكتساب المزيد من الرؤية في سلاسل التوريد الخاصة بهم واتخاذ خطوات ملموسة لمعالجة الانتهاكات - خاصة مع الزخم الإضافي الذي أضافته التشريعات الجديدة والقادمة المتعلقة بالعناية الواجبة في الولايات المتحدة والاتحاد الأوروبي.

الشكل هـ 1. تطور تصنيفات المصانع التي حددها المدققون الأخلاقيون التابعون لمعهد قطر لبحوث الحوكمة الأخلاقية، 2017-2022 (المصدر: بيانات نتائج تدقيق معهد قطر لبحوث الحوكمة)

الشكل هـ 2. النسبة المئوية للمصانع التي تعاني من حالات عدم الامتثال الحرجة حسب الفئة، 2019-2022 (المصدر: بيانات نتائج تدقيق إدارة الجودة والتحليل المالي)

في مشهد التوريد المتقلب الحالي، مرونة سلاسل التوريد تساوي المرونة في ظل مشهد التوريد المتقلب الحالي

يشير التنويع المتزايد باستمرار في سلاسل التوريد العالمية إلى أن العلامات التجارية وتجار التجزئة في طريقهم إلى تبني عدم اليقين باعتباره المعيار الجديد للتوريد العالمي. ومع استمرار مجموعة متنوعة من الاضطرابات في سلاسل التوريد في زعزعة مشهد التوريد العالمي، فإن الشركات التي تعطي الأولوية للمرونة والقدرة على التكيف في استراتيجية سلسلة التوريد الخاصة بها ستكون في أفضل وضع لتجاوز الاضطرابات.

الاتصال بالصحافة

البريد الإلكتروني: press@qima.com

شارك هذا على